The Data That Shows Asymmetric Learning Is Winning: Why Biotechs Now Bear the Clinical Trial Load

In 2020 I wrote about asymmetric learning as the quiet edge behind some of the biggest successes in biopharma. The core idea was simple: the companies that win aren’t the ones who predict best or de‑risk earliest. They’re the ones willing to explore more, ask better questions earlier, and place many small, high‑upside bets before the world forces symmetry on them.

Five years later, the data isn’t just supportive - it’s overwhelming.

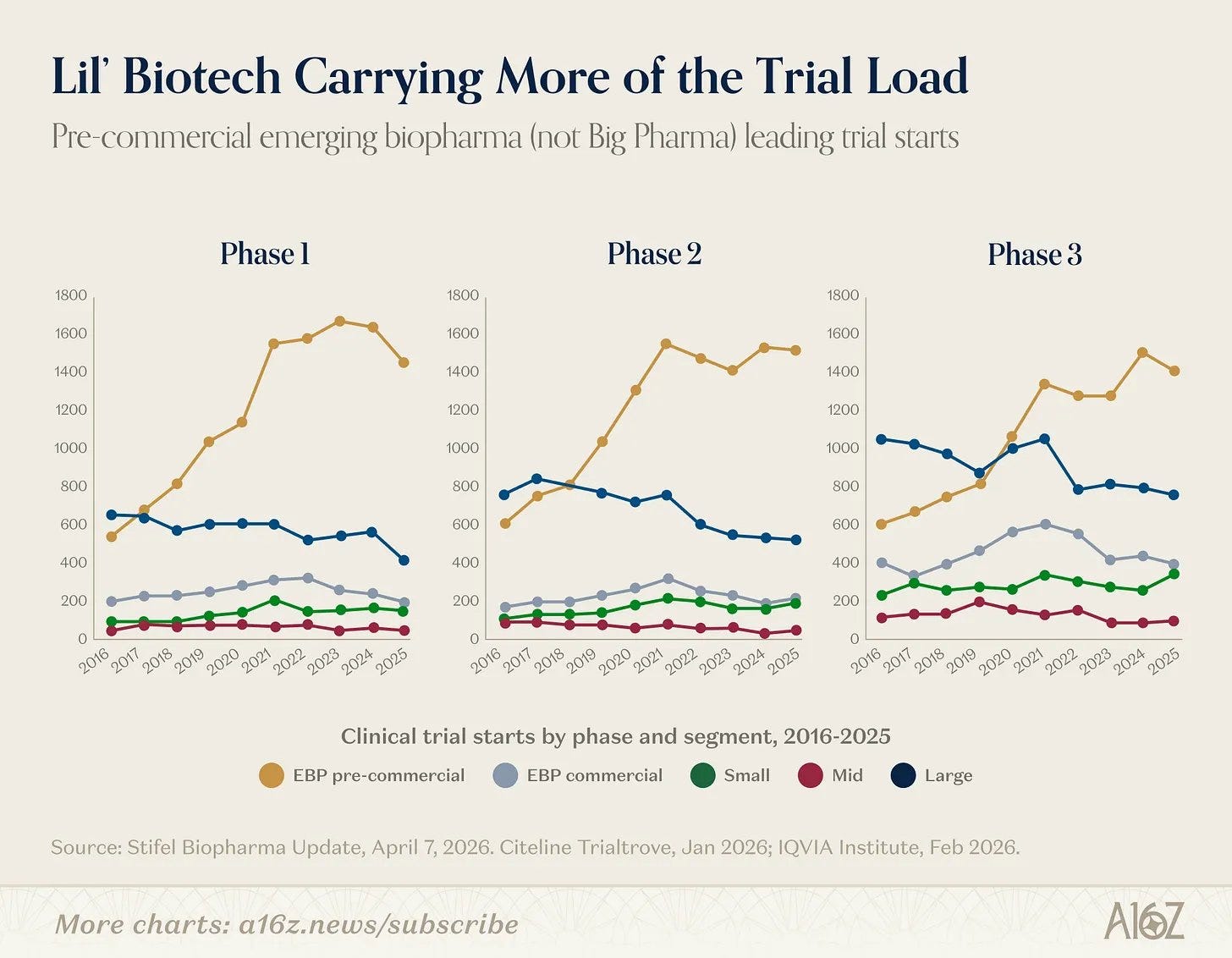

Pre‑commercial emerging biopharma companies (the “lil’ biotech” in the chart caption) have taken over clinical trial starts across every phase. They’re not just participating. They’re leading.

Here’s the chart, from A16Z:

Key takeaways from the 2016–2025 data (Stifel / Citeline / IQVIA):

Phase 1 - pre‑commercial EBP (‘emerging biopharma’, gold line) grew heavily from ~500 starts to peaks above 1,600, while Large Pharma (dark blue) declined.

Phase 2 - similar story: “lil’ biotech” surging, big players flat‑to‑down. (I’m not a fan of the phrase “lil’ biotech’ so will stop using it now…)

Phase 3 - even in late stage, pre‑commercial EBP now outpaces Large Pharma.

(The chart shows, but A16Z doesn’t speculate on, the dip post 2023… Small pharma seems to have picked up some, but not all, of it…)

Across all phases, pre‑commercial EBP companies accounted for the majority of trial starts in recent years, with their share rising from around the low‑40s percent in the mid‑2010s to roughly two‑thirds by the early 2020s in several datasets.

This probably isn’t a blip. It looks more like a structural shift.

What Asymmetric Learning Looks Like in Practice

Asymmetric learning favours exploration over exploitation in the early phases. You spend time and capital to generate optionality - multiple shots on goal, rapid iteration on signals, and a willingness to kill ideas fast and pivot.

Small biotechs are structurally built for this:

One big success changes everything (asymmetric upside).

Limited infrastructure means lower fixed costs and less pressure to protect an existing core.

Funding models reward bold exploration - until they don’t.

Decision rights sit closer to the science.

Large Pharma, by contrast, has optimised for symmetric learning: predictable returns, portfolio balancing, quarterly discipline, risk committees, and huge legacy operations that punish failure more visibly. The result - fewer early bets, more in‑licensing later, and a flatter line on the charts above.

This isn’t about “big companies are dumb”. It’s about incentives and architecture. When your organisation is built for reliability at scale rather than exploration, the rational move is to let someone else carry the exploration load - then acquire or partner once the asymmetry has been resolved into clearer probabilities.

The market seems to have noticed. Licensing deals, acquisitions, and platform valuations all reflect exactly this dynamic.

Why This Matters, Beyond the Numbers

The chart isn’t just about trial volume. It’s evidence that the locus of innovation has shifted towards organisations that can tolerate - and even seek - asymmetry.

It raises hard questions for anyone running (or investing in) large R&D organisations:

How do you rebuild exploration capacity without blowing up efficiency metrics?

Can you create “biotech” pockets inside a large company that are truly protected from symmetric pressures?

Or is the winning model now permanent specialisation - EBP explores, Big Pharma scales and commercialises?

Some large players, such as Lilly, are experimenting - venture arms, separate discovery units, aggressive external innovation mandates. But the aggregate data suggests it’s not yet moving the needle on raw trial starts.

The Deeper Lesson for All of Us

Asymmetric learning was never only a biopharma concept. It applies to strategy in any uncertain domain - tech, climate, personal careers. The pattern is the same: early variance creates later advantage. The organisations (and people) that win are often the ones willing to look inefficient for a while.

The biotech surge shows the power of that approach at industry scale. It also shows the limits of pure symmetry.

Big Pharma isn’t going away - its strengths in late‑stage execution, manufacturing, and global access remain critical. Commercial at obesity market scale still needs big organisations and budgets. But the data make one thing clear - if you want to lead in discovery and early development, you need to get comfortable carrying more of the exploration load yourself.

Or get very good at partnering with those who do.

Sources: Stifel Biopharma Update, Citeline Trialtrove, IQVIA Institute reports.